Mortgage Broker Commission Structures: Key Differences 2026

Key Takeaways:

- Most mortgage brokers earn through lender-paid commissions (upfront and trailing), not client fees

- Franchise brokers typically split commissions 30-50% with franchisors, while independents keep more

- Commission structures vary by lender but typically range from 0.6-0.7% upfront and 0.15-0.2% trailing

- Ask your broker about their earning structure and any client fees to ensure transparency

When you’re navigating the mortgage landscape, understanding how mortgage broker commission structures work can help you make better decisions about who to work with. The reality is that not all brokers are paid the same way, and these differences can impact the service you receive and potentially the recommendations you get.

The mortgage broking industry operates on various commission models, and as a borrower, you deserve to know exactly how your broker earns their income. This transparency isn’t just good practice, it’s actually required by law under Australia’s Best Interests Duty regulations.

How Do Mortgage Brokers Actually Get Paid?

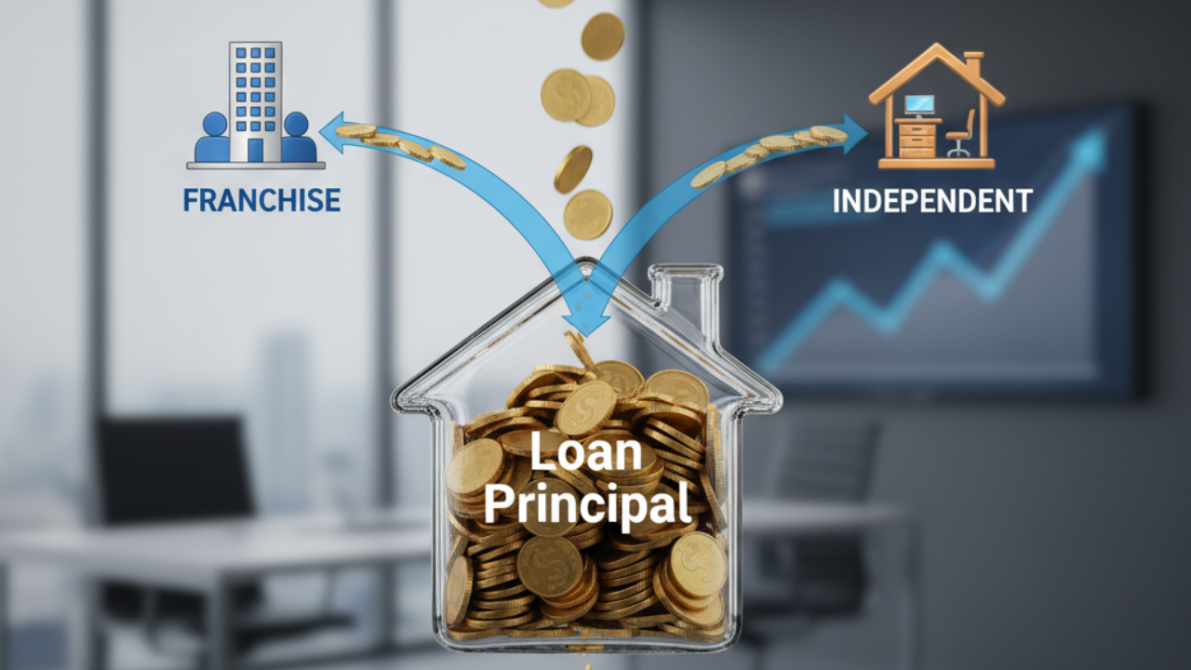

The foundation of mortgage broker commission structures revolves around two main types of payments from lenders: upfront commissions and trailing commissions. When your loan settles, lenders typically pay brokers an upfront commission of around 0.6-0.7% of the loan amount. On a $500,000 loan, this means roughly $3,000-$3,500 upfront.

But that’s just the beginning. Trailing commissions provide ongoing income, usually around 0.15-0.2% annually of the outstanding loan balance. Using our $500,000 example, that’s approximately $750-$1,000 in the first year, decreasing as you pay down the loan.

However, how much of this commission actually ends up in your broker’s pocket depends entirely on their business structure. This is where the key differences emerge.

Franchise vs Independent: The Commission Split Reality

Franchise Brokers: Sharing the Pie

If your broker operates under a major franchise like Aussie Home Loans or Mortgage Choice, they’re typically splitting their commission with the franchisor. These splits can range from 30-50% going to the franchise, leaving the individual broker with 50-70% of the total commission.

On that $500,000 loan example, a franchise broker might receive $1,500-$2,450 upfront instead of the full $3,500. The trailing commission gets split the same way, meaning $375-$700 annually instead of the full amount.

Why do brokers accept these arrangements? Franchises provide brand recognition, marketing support, compliance systems, and ongoing training. For many brokers, especially those starting out, this trade-off makes sense.

Independent Brokers: Keeping More, Paying More

Independent brokers typically keep closer to 100% of their commission, but they have higher operating costs. They need to pay for their own marketing, compliance systems, professional indemnity insurance, and aggregator fees for lender access.

Aggregator fees, the cost of accessing lender panels, can range from $300-$800 monthly, plus percentage-based fees on loan volumes. So while independents keep more commission, their overheads are significantly higher.

The Aggregator Factor: Another Layer of Commission Sharing

Most brokers, whether franchise or independent, work through aggregators to access lender panels. Types of mortgage broker commissions can be further complicated by aggregator arrangements:

- Bank-owned aggregators (like Aussie, which is owned by CBA) may offer different commission structures

- Independent aggregators like AFG or Connective typically charge membership and volume-based fees

- Some aggregators offer higher commission rates for higher volumes, creating tiered structures

These arrangements mean that even “independent” brokers may not be keeping 100% of their commission after paying aggregator fees.

Client Fees: When Brokers Charge You Directly

While most brokers don’t charge clients directly, there are exceptions to be aware of:

Upfront Fees Some brokers charge application fees ranging from $200-$995, though these are often refunded at settlement. This practice has become less common, with about 85% of brokerages now operating on a “no fee to client” model.

Clawback Recovery Fees If you refinance within 18-24 months, lenders often “clawback” the upfront commission from brokers. Some brokers pass this cost to clients through clawback clauses in their agreements. Not all brokers enforce these clauses, but it’s worth asking about.

Complex Situation Fees For particularly complex applications requiring extensive work, some brokers may charge hourly consultation fees. These should always be disclosed upfront and agreed to in writing.

How Commission Structures Impact Your Experience

Understanding mortgage broker commission structures matters because it can influence the service you receive:

High-Commission Lenders While regulations require brokers to act in your best interests, lenders with slightly higher commission rates might get more attention. However, recent regulatory changes have standardised commission rates across most major lenders to minimise this risk.

Volume-Based Bonuses Some lenders offer volume bonuses to brokers who write a certain number of loans. While these are less common than previously, they can create incentives to prioritise speed over thoroughness.

Trail Commission Incentives The ongoing nature of trail commissions means brokers have an incentive to keep you satisfied long-term. Many brokers provide annual loan reviews and refinancing advice specifically because they continue earning trail commission.

Regional Variations: How Location Affects Commission Structures

Commission percentages remain consistent across Australia, but the dollar amounts vary significantly based on local property values:

Sydney and Melbourne Brokers With average first-home buyer loans around $625,000 in NSW, brokers in these markets earn higher dollar amounts per transaction. A 0.65% upfront commission on a $625,000 loan equals $4,062, plus approximately $937 annually in trail commission.

Adelaide and Perth Markets Lower average loan amounts (around $400,000-$450,000) mean proportionally lower commission dollars, but brokers often compensate by handling higher transaction volumes or focusing on repeat clients and referrals.

The Regulatory Framework: Best Interests Duty

Since January 2021, all mortgage brokers must comply with the Best Interests Duty, regardless of their commission structure. This means:

- Brokers must prioritise your needs over commission considerations

- All commission arrangements must be disclosed in writing

- Brokers must document why they recommended specific loans

- You have access to free dispute resolution through AFCA if issues arise

What to Ask Your Broker About Their Commission Structure

When engaging a mortgage broker, ask these specific questions:

- “Do you charge me any fees directly, and under what circumstances?”

- “What percentage of your commission do you keep versus what goes to your franchise or aggregator?”

- “Do different lenders pay you different commission rates?”

- “Do you have any clawback clauses if I refinance early?”

- “What ongoing services do you provide after settlement?”

A professional broker should answer these questions transparently and provide written disclosure of their commission arrangements.

Making Informed Decisions About Mortgage Broker Commission Structures

The key isn’t necessarily to find the broker with the lowest commission costs, since you typically don’t pay these directly anyway. Instead, focus on:

Let me share a quick story from my own homebuying journey that drives this home. When I was a first-time investor, commission structures were honestly the last thing on my mind. I only discovered at settlement that my broker, Laura, was part of a major franchise and shared almost half her commission with the brand. My initial reaction? Worry that maybe I’d paid ‘too much’ somehow, or missed out on a better deal. But what really struck me was what happened next: Laura was relentless in her support scheduling annual check-ins, flagging when better rates appeared, and even guiding me through a tricky refinance years later (without ever charging hidden fees or pushing unnecessary products). I realised that her split commission didn’t mean less value for me, in fact, when she explained her franchise offered powerful compliance tools and access to an unusual lender panel, it all made sense. For me, the true value lay in her transparency and ongoing commitment, not the exact breakdown of her commission statement. It was a real-life lesson that the best brokers are defined not by how much they keep, but by how much they keep showing up for you.

Value for Service A franchise broker splitting commissions might still provide better value through superior systems, faster processing, or better lender relationships than an independent broker keeping 100% but lacking resources.

Transparency and Communication Regardless of commission structure, the best brokers are transparent about their earnings and maintain regular communication throughout and after your loan process.

Long-term Relationship Since brokers earn trail commission, they have incentives to maintain long-term relationships. Look for brokers who offer annual reviews and proactive refinancing advice.

The Future of Mortgage Broker Commission Structures

The industry continues evolving, with some trends worth noting:

Increased Transparency Requirements Regulators are pushing for even greater commission disclosure, making it easier for consumers to understand how their broker is paid.

Fee-for-Service Models A small but growing number of brokers operate on fee-for-service models, where they charge clients directly and rebate lender commissions. This eliminates potential conflicts but requires upfront payment from borrowers.

Technology Integration Digital platforms are enabling new commission-sharing arrangements and potentially lowering the overall cost of mortgage broking services.

Understanding mortgage broker commission structures empowers you to make informed decisions when choosing professional mortgage assistance. While the specific commission arrangements vary between franchise and independent brokers, the key is finding someone who provides transparent service and genuine value.

Remember, according to insights from PropertyChat.ai, most brokers earn through upfront commissions around 0.6-0.7% of the loan amount plus trailing commissions of 0.15-0.2% annually. Franchise brokers typically share 30-50% with their franchisor, while independents keep more but pay higher operating costs.

The most important factor isn’t how your broker gets paid, but whether they’re acting in your best interests and providing value for their service. By asking the right questions and understanding the commission landscape, you can choose a broker who will serve you well throughout your property journey.

For more detailed guidance on property investment and mortgage strategies, consider exploring the comprehensive resources available through PropertyChat.ai, which draws from 20 years of practical experience in property investing, mortgage broking, and renovation advice.

Suggested Articles

Positive vs Negative Gearing: Key Differences Explained

Understanding the Mortgage Broker Service

How to Pay Off Your Mortgage Faster

Who Can Witness a QLD Mortgage

This article is provided in line with the Brand Voice of PropertyChat and Your Property Success, emphasising trust, actionable advice, and long-term partnership in property finance.

Transcript

How Mortgage Brokers REALLY Get Paid in 2026 Explained!

0:00Welcome to the explainer. So, you’re

0:02looking to buy a home and you’ve

0:03probably heard that using a mortgage

0:04broker is completely free. But is that

0:06really the whole story? Today, we’re

0:08going to pull back the curtain and see

0:09exactly how your broker gets paid and

0:11more importantly, what it all means for

0:12you. So, let’s get right to it. Is your

0:15broker really working for free? I mean,

0:18it sounds amazing, right? But while you

0:20might not be writing them a check

0:22directly, that money has to come from

0:23somewhere. So, let’s break down where

0:25their commission actually comes from.

0:28Okay, first up, let’s cover the absolute

0:30basics of how brokers get paid. The most

0:33important thing you need to know is

0:34this. In nearly every single case, it’s

0:37the lender, the bank, that pays the

0:39broker’s commission, not you. And that

0:41payment is generally broken down into

0:42two main types. You’ve got the upfront

0:44commission, which is a one-time lump sum

0:46payment that happens right when your

0:47loan settles. And then there’s the

0:49trailing commission, which is a smaller

0:50ongoing payment that they receive for

0:52the life of a loan. Let’s put some real

0:54numbers to this, shall we? That upfront

0:56commission is typically somewhere

0:58between 6% and.7% of your total loan

1:01amount. You can think of this as the

1:03broker’s main payday for doing all that

1:05heavy lifting to get your loan approved.

1:07And what about that trailing commission?

1:10Well, that’s an annual payment of around

1:120.15% to 2% of whatever your loan

1:15balance is at the time. The whole idea

1:18here is to give brokers an incentive to

1:20provide you with long-term service and

1:22make sure your loan is still the right

1:23fit for you years down the track.

1:25Okay, I get it. Percentages can feel a

1:28little abstract, right? So, let’s make

1:30this super concrete with a really common

1:32scenario, a $500,000 home loan. So, for

1:35that half a million loan, you can see

1:36the upfront commission would land

1:38somewhere between $3,000 and $3,500.

1:41Then, the trailing commission would add

1:42another $750 to a,000 bucks in that

1:44first year. But, and this is a really

1:47big butt, that gross amount is almost

1:49never what the individual broker

1:50actually takes home. And that brings us

1:53to probably the biggest factor affecting

1:55a broker’s real income. It’s all about

1:57the difference between franchise and

1:59independent brokers because their

2:01business model completely changes how

2:03that commission gets sliced up. You see,

2:06if your broker is part of a large

2:08well-known franchise, they don’t get to

2:09keep that whole commission pie. This

2:12chart shows a pretty typical split where

2:14the franchise itself can take a hefty

2:16slice. We’re talking 30%, sometimes up

2:19to 50% of the earnings. and they get

2:21that in exchange for providing brand

2:23recognition, marketing, and all that

2:24back office support. Now, on the flip

2:26side, you’ve got your independent

2:28broker. They get to keep a much, much

2:30bigger piece of the pie, often around

2:3295%. But here’s the catch. They’re on

2:34the hook for all their own operating

2:36costs. Everything from marketing and

2:38insurance to something called aggregator

2:40fees, which is what they pay just to get

2:42access to a wide panel of lenders. So,

2:45you see the trade-off, right? Franchise

2:47brokers get a ton of support, but they

2:49take home a smaller cut. Independent

2:51brokers get a much bigger slice of the

2:53commission, but they have to foot the

2:55bill for everything themselves. This is

2:57one of the biggest differences in

2:58commission structures out there, and

2:59it’s so important to understand. Okay,

3:02so we’ve established the lender usually

3:04pays the broker, but are there any

3:07exceptions? Are there loopholes? Well,

3:09yes, there are a few. So, let’s talk

3:11about the rare times when you, the

3:14borrower, might actually be asked to pay

3:15a fee directly. You might come across an

3:18upfront application fee, though honestly

3:20those are often refunded later. A more

3:22serious one to watch out for is a

3:24clawback fee. This can happen if you

3:26refinance your loan too early and the

3:28lender literally claws back the

3:30commission from your broker. And for

3:31really complex situations, some might

3:33charge a special fee for the extra work.

3:35But the key thing is these must always

3:37be disclosed to you right at the start.

3:39No surprises. But I really want to

3:41stress you shouldn’t lose sleep over

3:43these fees. They’re becoming pretty

3:44uncommon. In fact, right now about 85%

3:48of Australian brokerages operate on

3:49what’s called a no fee to client model.

3:52So the chances of you having to pay one

3:53of these fees are actually quite low.

3:56All right, so we get the mechanics now.

3:58We know how the money flows. But the big

3:59question is how does all of this

4:01actually affect you? Let’s connect the

4:03dots between these commission structures

4:05and your actual experience as a

4:07borrower. This right here, this is your

4:09single most important protection. It’s

4:11called the best interests duty. It’s a

4:14legal requirement that forces brokers to

4:16prioritize your financial needs above

4:18their own commission. It means they

4:20can’t just recommend a loan because it

4:22pays them more. They have to document

4:24and justify why a specific loan is

4:26genuinely the right one for you. To see

4:28how this all plays out in the real

4:30world, let’s look at a story from one

4:32home buyer. They said, “I only

4:34discovered at settlement that my broker

4:36shared almost half her commission.” Now,

4:38you can imagine how hearing that might

4:39cause you a little bit of concern,

4:41right? But then this happened. The story

4:44continues. Laura was relentless in her

4:46support, scheduling annual check-ins,

4:48flagging when better rates appeared, and

4:51this completely changed their whole

4:53perspective. And that right there is the

4:56real takeaway from this whole explainer.

4:58The commission split doesn’t actually

5:00determine the value you receive. The

5:03real value comes from the broker’s

5:04expertise, their transparency, and their

5:07commitment to you long, long after the

5:09loan is settled. So, how do you find a

5:11broker who provides that kind of amazing

5:13value? It’s simple. You have to ask the

5:16right questions. This next part is your

5:18toolkit to make sure you get complete

5:20transparency. Here they are. Think of

5:22this as your essential checklist. Ask

5:25them, one, do you charge any fees

5:27directly to me? Two, what is your

5:29commission split? Don’t be afraid to

5:31ask. Three, do different lenders on your

5:34panel pay different rates? Four, do you

5:36have a clawback clause I should know

5:38about? And five, maybe the most

5:40important of all, what ongoing services

5:42do you provide after my loan settles? A

5:45great broker will be happy, even proud

5:47to answer these clearly and confidently.

5:49So, we’ve covered a lot of ground. We’ve

5:51demystified how commissions work, and

5:53you now have the exact questions you

5:55need to ask. So, what’s the smartest

5:57next step you can take on your property

5:59journey? Look, understanding how your

6:01broker gets paid is all about empowering

6:03you to make a smarter choice. To keep

6:05learning and get expert guidance for

6:07every single stage of your property

6:08journey, from finding a great broker to

6:10securing the right loan, visit property

6:13chat.ai. It’s your complete resource for

6:15navigating the market with total

6:17confidence.

Frequently Asked Questions

Do I have to pay mortgage broker fees if they work on commission?

In most cases, no. About 85% of brokers charge clients zero fees, earning their income entirely through lender-paid commissions. However, some brokers may charge fees for complex situations or very small loans, which should be disclosed upfront.

Why do franchise brokers earn less commission than independent brokers?

Franchise brokers typically split their commission 30-50% with their franchisor in exchange for brand support, marketing, compliance systems, and training. Independent brokers keep more commission but have higher operating costs including aggregator fees, insurance, and marketing expenses.

Can mortgage broker commission structures influence loan recommendations?

While commission rates are now largely standardised across major lenders to prevent bias, the Best Interests Duty legally requires brokers to prioritise your needs over their commission. Brokers must disclose their earnings and document why they recommended specific loans

What happens to trailing commissions if I refinance with a different broker?

Trail commissions stop when you refinance to a different lender. If you use the same broker for your refinance, they may earn a new upfront commission. Some brokers have clawback clauses requiring you to pay back lost commissions if you refinance very early, typically within 18-24 months.